It also should be noted that this entry is the only one made during the year to the Bad Debt Expense account. That is to say, if other factors can make one prediction better (such as total sales, general economic conditions, or geographic region), we should use them if they are easily included. They rely on the accrual approach, which calls for recognizing revenue when the seller performs.

Uncollectible Accounts Receivable

Using the allowance method, complying with the matching principle, the amount is recorded in the current accounting period with the following percentage of credit sales method journal. This expense is called bad debt expenses, and they are generally classified as sales and general administrative expense. Though part of an entry for bad debt expense resides on the balance sheet, bad debt expense is posted to the income statement.

Fundamentals of Bad Debt Expenses and Allowances for Doubtful

Another title for this account is Bad Debt Expense, This account is closed to Income Summary and is generally shown as a selling expense on the income statement. An estimate is required because it is impossible to know with certainty which accounts outstanding at the end of the year will become uncollectible during the next year. Explore the role of FASB in financial reporting, including its mission, standards, and collaboration for consistency in accounting practices.

Collections

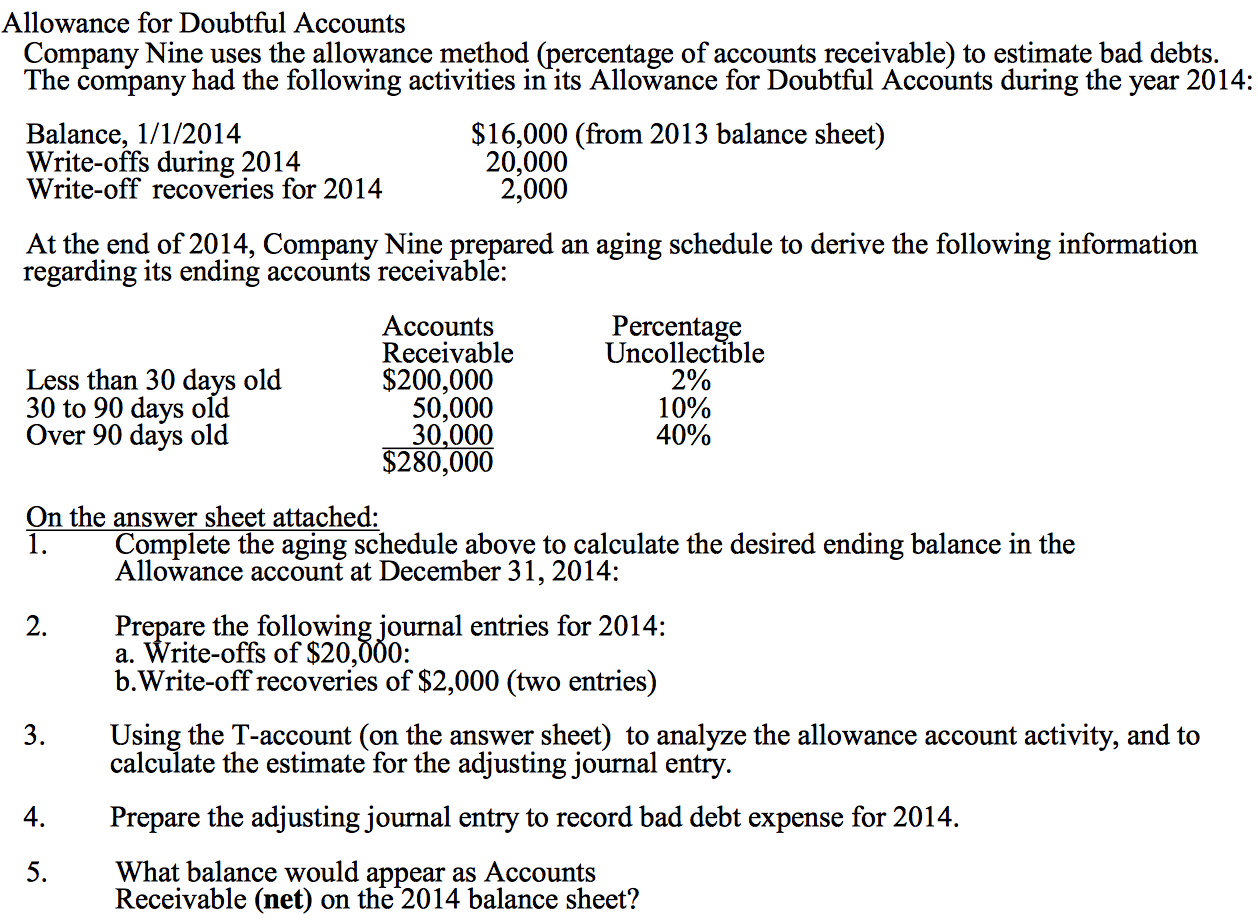

Offer your customers payment terms like Net 30 and Net 15—eventually you’ll run into a customer who either can’t or won’t pay you. When money your customers owe you becomes uncollectible like this, we call that bad debt (or a doubtful debt). The sum of the estimated amounts for all categories yields the total estimated amount uncollectible and is the desired credit balance (the target) in the Allowance for Uncollectible Accounts.

- Uncollectible accounts arise in the normal course of business and are an inherent risk of extending credit to customers.

- The first entry reverses the bad debt write-off by increasing Accounts Receivable (debit) and decreasing Bad Debt Expense (credit) for the amount recovered.

- The action does not affect either the net amount of accounts receivable or the bad debt expense.

- We may earn a commission when you click on a link or make a purchase through the links on our site.

- The allowance method is the more widely used method because it satisfies the matching principle.

- This action removes the uncollectible receivables from the accounts receivable balance.

Relevant Accounting Standards and Literature

Once this account is identified as uncollectible, the company will record a reduction to the customer’s accounts receivable and an increase to bad debt expense for the exact amount uncollectible. Here, we’ll go over exactly what bad debt expenses are, where to find them on your financial statements, how to calculate your bad debts, and how to record bad debt expenses properly in your bookkeeping. By following these guidelines and best practices, companies can improve their estimation of uncollectible accounts, enhance financial reporting accuracy, and maintain strong financial health.

Bad Debt Expense increases (debit), and Allowance for Doubtful Accounts increases (credit) for $22,911.50 ($458,230 × 5%). Let’s say that on April 8, it was determined that Customer Robert Craft’s account was uncollectible in the amount of $5,000. If you don’t have a lot of bad debts, you’ll probably write them off on a case-by-case basis, once it becomes clear that a customer can’t or won’t pay. Generally Accepted Accounting Principles (GAAP) are a set of rules and standards established to ensure consistency, transparency, and comparability in financial reporting across all industries in the United States.

Common reasons for uncollectible accounts include the customer’s bankruptcy, financial difficulties, or disputes over the goods or services provided. Percentage-of-receivables method The percentage-of-receivables method estimates uncollectible accounts by determining the desired size of the Allowance for Uncollectible Accounts. Rankin would multiply the ending balance in Accounts Receivable by a rate (or rates) based on its uncollectible accounts experience. In the percentage-of-receivables method, the company may use either an overall rate or a different rate for each age category of receivables. Uncollectible accounts expense is recorded by debiting bad debt Expense and crediting the allowance for uncollectible accounts. To illustrate, let’s continue to use Billie’s WatercraftWarehouse (BWW) as the example.

This is different from the last journal entry, where bad debtwas estimated at $58,097. That journal entry assumed a zero balancein Allowance for Doubtful Accounts from the nonrefundable prior period. Thisjournal entry takes into account a debit balance of $20,000 andadds the prior period’s balance to the estimated balance of $58,097in the current period.

The specific identity and the actual amount of these bad accounts will probably not be known for several months. No physical evidence exists at the time of sale to indicate which will become worthless (buyers rarely make a purchase and then immediately declare bankruptcy or leave town). For convenience, accountants wait until financial statements are to be produced before making their estimation of net realizable value. Notice that bad debt expense in this case is simply the other half of the entry to get the balance sheet account adjusted. The focus in this case is on the net realizable value of the receivables, and the income statement (bad debt expense) is relegated to second place. As of January 1, 2018, GAAP requires a change in how health-care entities record bad debt expense.